Should I Retire to Go Travel in 2026?

I keep redoing the calculations, over and over and over again. I calculate based on my entire net worth. Then, I calculate with guardrails and limiting parameters.

I end up staring at my results for a very long time. The math – those cold, hard numbers – are, this time, uncharacteristically assuring to the extreme. No matter how I slice it, I can quit my job right now and go travel the world while living off a very conservative $2,000 per month.

World travel is a serious part of my life plans; I just didn’t expect I’d consider starting it in 2026. I also didn’t expect the premier retirement financials expert to come out with new research that paints an even rosier picture than planned. Nor that the appeal of leaving fascism behind would bump my timeline way, way up. Life sure is full of surprises, and that’s why life requires me to think through opportunities that the FIRE movement makes possible for me.

How I Calculated My Potential Yearly Budget

I’ve got a basic formula of determining a budget from years of financial independence articles percolating in my head. That basic formula for understanding how much money you can safely spend in retirement is as follows:

SafePercentage x AmountOfMoney = YearlyBudget

YearlyBudget / 12 = MonthlyBudget

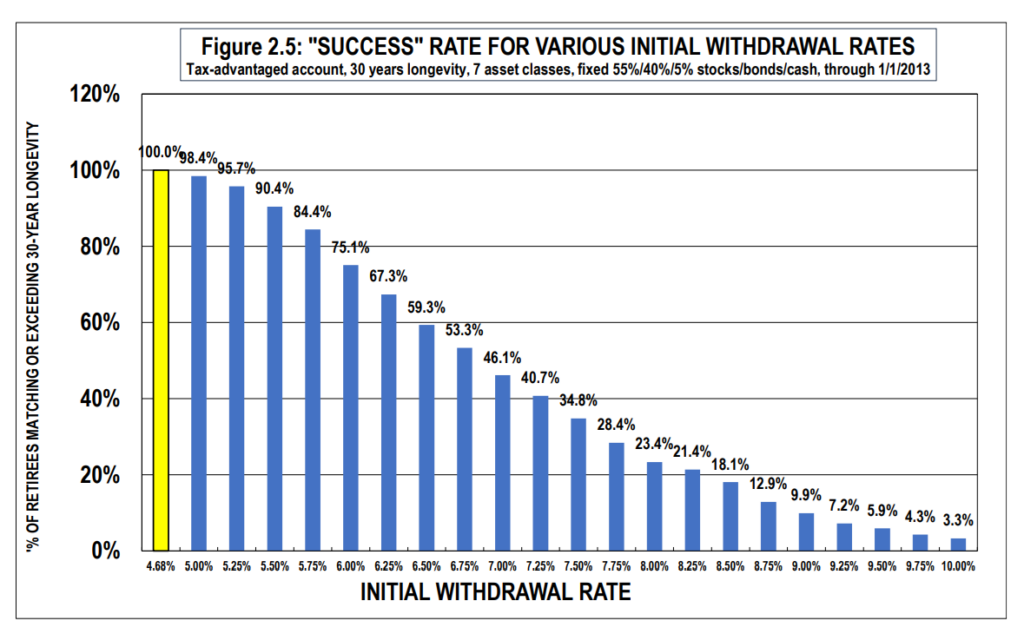

The “SafePercentage” default is 4% given the 4% Rule (of thumb). That is already a more conservative estimate than what academic experts have uncovered; the REAL default, based on historical averages, is actually 4.68%. That secondary number is also conservative, by the way, as it is including the most catastrophic economic meltdowns in the last century. In other words, 4.68% is the withdrawal rate at which will be sufficient 100% of the time for a 30-year retirement timeline. The data also shows that, even with those catastrophic meltdowns, a 5% rate will be sufficient 98.4% of the time:

My SafePercentage is a little different, in that I’ve simplified the asset classes and allocation. My formula assumes the AmountOfMoneyInvested is all invested in index funds that track the overall stock market, aka total stock market index funds. Index funds that track a large number of the top performing, like ones tracking the Dow Jones or S&P 500, work fine enough for this too.

Some folks use their entire net worth for this number, not only including index fund investments but also bonds, cash, home equity, and alternative investments like risky stocks, crypto, collectibles, what have you. I don’t count possessions like my car in my net worth, but I do count cash, crypto, and government bonds. That would put my total net worth at about $660k as of the time of this writing. Counting my index fund investments only, I am at roughly $625k as of the time of this writing.

The Withdrawal Percentages

If we use that $625k figure, a MonthlyBudget of $2k shows a ridiculously conservative SafePercentage of 3.84%. It gives me a little wiggle room for any small unexpected or emergency expenses, which I don’t strictly need anyway as I have an emergency fund for scenarios like that. If I were to assume 4.68% would work for me, my safe MonthlyBudget can go up to $2,450 (using 4.68% of my index funds investments only, rounded up a bit). Even using 4% on my $625k funds gives me a $1,000 surplus for whatever I may need. Chart below for a better visualization:

| Withdrawal Rate | Annual Amount (based on $625k) | Monthly Amount |

| 4.68% | $29,250 | $2,437 |

| 4.15% | $25,937 | $2,161 |

| 4.00% | $25,000 | $2,083 |

| 3.84% | $24,000 | $2,000 |

At most, I would only go up to 4.15% instead of 4.68%. Bill Bengen, the premier retirement finances expert, mentions that’s roughly the ideal for a 50-year retirement.

The question now is: can I actually live off of $2k a month? The answer is: only if I am willing and able to change my current geographic location. And I totally can! With my Irish citizenship, I can live anywhere in the European Union indefinitely. Lucky me!

What Makes Europe Doable

A lot of policies throughout the centuries have lined up to make me able to do this in 2026. The EU Charter and Schengen Agreement enshrine the rights of any EU citizen to live virtually anywhere on the continent WITH low-cost health care in the bargain. Irish law codified my right to citizenship by descent through my Irish-born grandparents, as well as my right to live anywhere in the UK to boot if I so wish.

And centuries of colonialism by mainland European countries has poured a disproportionate amount of wealth into European cities, generating cost-of-living advances paid for with blood and malice. (Included here because it’s not good in the long run to ignore atrocities, especially when the consequences are still heavily present.)

With the legal and socioeconomic acknowledgements above, the only other potential barriers to making this doable are financial and logistical. Both of these, too, are soundly taken care of.

For one, Europe has world-class destinations that are cheaper than what I’m used to in the US. The Earth Awaits estimates a lean budget in Los Angeles is $3,771 a month, and a lean budget just outside of Boston is $3,806 a month. Both these estimates are right in line with my experience living in both areas, so I trust their budgetary estimates. Imagine my surprise to learn I can live in gorgeous – and popular! – cities in Europe on the lean budget I’m used to! With a 4.15% withdrawal rate, I can afford Prague, Lyon, Porto, Genoa, Athens, Sicily, and Sevilla.

The numbers, for reference:

| City | Monthly Budget Amount |

| PRAGUE, Czech Republic | $2,148 |

| LYON, France | $1,929 |

| PORTO, Portugal | $1,869 |

| GENOA, Italy | $1,818 |

| ATHENS, Greece | $1,581 |

| CATANIA, Sicily, Italy | $1,457 |

| SEVILLA, Spain | $1,228 |

Bumping my budget up to 4.68% leaves me sitting pretty in Venice, Rome, Madrid, Vienna, and Barcelona. And all of these are just the cities at the top of the budget; I’ve included a lot of cities I’m interested in on the chart below to demonstrate:

More cities here, too!

| City | Monthly Budget Amount |

| ROME, Italy | $2,372 |

| VENICE, Italy | $2,359 |

| BARCELONA, Spain | $2,355 |

| MADRID, Spain | $2,342 |

| VIENNA, Austria | $2,328 |

| BOLOGNA, Italy | $2,148 |

| SPLIT, Croatia | $1,929 |

| MODENA, Italy | $1,869 |

| WARSAW, Poland | $1,818 |

| HERAKLION, Crete, Greece | $1,578 |

| CORDOBA, Spain | $1,457 |

| BUCHAREST, Romania | $1,228 |

Logistically, my top concerns would be travel accommodations and housing. Thanks to the Internet, I can secure monthlong stays within just a few minutes. Plus, the EU has infrastructure leagues ahead of America. I will not need to rely on a car while in Europe to travel about. Trains on trains FTW!!!

This may seem risky. I don’t think so. “The best laid plans of mice and men oft go awry” may very well be true for me despite my backup plans, resources, and out-of-the-box thinking. What I do know is that I feel good about my planning. I have confidence in my own tenacity to ensure I am taken care of. It’s gotten me through a violent childhood, college, and corporate America, in that order. I have faith it will also get me through slow travel for some time through Europe.

As established above, I can very safely spend $2,000 a month, or $24,000 a year, with my current nest egg. In fact, I may be able to spend up to $29,250 a year without ever running out of money (so $750 less than my original calculations in September). That is assuming I do not work at all and rely solely on my investments to fund my living expenses.

But I can definitely work without issue if need be.

Thanks to my Irish citizenship, I can work anywhere in the EU. (I used “retire” in the headline just to make it catchy, so please don’t drag the retirement police into this.) At the very least, I would still be working, just not for money. Writing would become my top priority for the first time ever, now that I have neither school or a full-time job to dedicate the bulk of my time and energy towards. It would be spectacular if my future completed writing projects will generate money, thus making me a paid worker again. But I don’t need to be paid to do it, unlike my jobs in marketing.

I may choose to work part-time for a few months for an extra spending buffer, which can be anything I’ve done before I know I wouldn’t mind:

- A temp marketing role

- An English language tutor or substitute teacher

- A receptionist

- A Workaway laborer

- By flipping furniture or other gig-type jobs

If I really need to make up more money in the original estimated budget, I am still of able mind and body and can earn it. I doubt I’ll have a tough time finding work. Even if I do, $30k will make up 4.8% of my nest egg. That could very well prove a successful withdrawal rate, and I can always live in areas with a lower cost of living to put this back to rights.

If I DO find it hard to find work?

Then I’ll simply wait it out. I have enough money invested in my taxable account alone to fund me for the next decade or so with little to no investment growth at all. I can wait long enough for jobs to open up again and let me build up another cushion.

Given all of this, I am ABSOLUTELY willing and able to change my geographic location. My monthlong travels to Europe in the last few years has only further confirmed I would delight in exploring foreign countries. And, well, I am horrified enough at the US government in 2025 to fly outta here with great relief.

Rejecting Fascism With My Feet

Europe has its own problems and threats. A big one is a potential war with Russia. Another is the rise of authoritarianism over there too, similar to what Americans are seeing here. That said, I consider them less threatening at this point in time than the actual fascism that is already here in America, not simply on the rise.

Via annefrank.org:

There was no room for anyone with different ideas; from the very beginning, opponents of the regime were intimidated, persecuted and imprisoned in concentration camps. Many political and cultural dissidents therefore quickly left the country, whether they were Jewish or not; this first wave of emigrants or refugees included many writers, journalists and artists.

Well, f***… see that word “writers”? Guess I fit the bill.

If I do leave, I’d reckon it would be sometime in May at the earliest. That gives me time to pad my cash cushion until then. Plus, my company typically pays out bonuses in mid-March, which is money I don’t have to leave on the table. I don’t think the country will implode in the next six months or so; it’s anything more than six months out I’m most wary of. So you heard it here first (outside of my last net worth update, I mean): I may be leaving the country next year for more peaceful pastures!

Who Yet Knows What the Future Holds!

Going this route is well off the beaten path even for my financial independence peers. My withdrawal rates are higher than the targets for many a FIRE forum commenter, not to mention with a lower nest egg than the million dollar benchmark. Less than two-thirds lower, if the markets don’t grow in 2026. I’d also become an early retiree before my 32nd birthday, which puts my ability to fund the rest of my life further into question given the longer retirement horizon.

If all of that wasn’t enough, I’d be doing it alone – without any significant others to split expenses with or relatives to leave me some future inheritance. The first reaction from seasoned FIRE folks is “WOW! How… brave? Couldn’t be me, though.” I don’t mind the skepticism. Personal finance is personal, so my specific financial outlook is going to look different from anyone else’s.

If I choose this path, and stick to it, then I’ll have to deal with extra investment management some years down the road. The bulk of my investments are in tax-advantaged accounts, so I’ll have to either play around with a Roth IRA conversion ladder or with Section 72(t) of the IRS code to access that money before the established retirement age. Wherever my life ends up, I’m set up well enough to weather it with a smile. Brave or not, I’ve got a New Year to plan for coming on up!

Cover image credit: PJ Gal-Szabo via Unsplash

If long term travel is part of your life goal, then there is no better time to do it now, at least for the next 3 years while Trump remain president. You would get to travel the world and do anything you want while you are still young and healthy enough to do it, instead of waiting until you are old, or settled down with spouse and kids and can no longer do it.

And if you still want to make money while abroad, instead of trying to find a low paying job abroad, can you just keep your current job since it is fully remote job?

I think 31 would be a great age to retire. You would be on par with MMM, who retired at 31 with 1.2M in today’s dollar between the 2 of them, and Millennial Revolution who retired at 31 with 1.3M in today’s dollar between the 2 of them. As a single person, you would be retiring with half of that amount, although a single person cannot have someone to split shared housing expense with, so your retirement will be leaner unless you are willing to have housemate. Purple retired at 30 with $678k in today’s dollar, but she has a working partner to split expenses with and to fall back on in case things go wrong, so it’s not really a fair comparison.

Hannah, thank you for such a thoughtful summary 🥰 You raised the bar with the net worth comparisons that account for inflation AND the nuances to boot. Would you mind if I added your comment to the main body of the article?

As for the jobs question: I did think about asking my bosses if I can work remotely abroad (much like I asked them in 2023 if I could work remotely from CA). Not like there’ll be much difference between me working from one different time zone to another different time zone, as you point out. I just bring up the work potential as my backup option should something go awry. Something that pays less, but only requires I work 1-2 days a week, would be preferable to something that pays more, but has me babysitting Slack and emails full time. If I do keep my job after a move abroad, I don’t think I’d keep it for more than a matter of months before resigning for real. It’s just not what I would most want to do with my time when I no longer need to.

That said, I’m kicking around the idea of offering to continue working for X number of months to help with handoffs. I’m the only person on our marketing team, if not the entire organization, who keeps important recurring tasks running smoothly; given that, I’m not sure they’d get someone new up to speed in the three-week notice I’d likely give. Maybe they’ll agree to let me work from abroad, maybe not. Either way, I’ve got enough now where the option to quit and travel is actually a viable one (and right as the most heinous evils are coming home to roost for the country, so to speak).

I hadn’t thought about how my nest egg compares to those others you brought up, and I literally have an article in the WWG archives analyzing those exact three early retirement bloggers. My aunts at All Options Considered already did a deep dive for me on the viability of doing it. Combined with your saying “hey, these other success stories retired on roughly the same amounts you’ll end up with” is the perfect external validation that this is feasible. 🫶

Ofc, feel free to add it in your post. I used those 3 fire bloggers because those are the one you used in your previous article, and tbh I keep going back to that article for a sanity check too, since nowadays the reddit FIRE community are full of “$5M at 50, planning to retire at 60” that I think are AI generated because capitalism would collapse if everyone was to pursue the original FIRE.

Comparision is the thief of joy, but I think you are doing just as great as those FIRE bloggers. If you were married like them, to another WeWantGuac, your net worth would be doubled to about 1.2M at 31 like their too.

I think if you don’t plan to work from abroad for long even if they let you, then you can just hand in your standard 2 weeks resignation 2 weeks before you move abroad, and let them know that you gotta move abroad in 2 weeks but if they let you work from abroad then you can stay until they find your replacement.

Great plug for your aunts lol! I think I came across the All Options Considered blog once before, but I didn’t know it was your aunts’ blog!

Yay, adding soon!! Along with a link to that article; I just reread it and went “oh yeah, this is emphatically relevant at this point in time”. I’ve also seen those insane posts of multi-millionaires feeling too uncomfortable to retire; I’ve always dismissed them as folks taking a fantasy of wealth a step too far, but those are the ones that see engagement so ¯\_(ツ)_/¯ Not sure if I’ll ever get married at this point, but if I ever do meet my WeWantGuac clone there’s no question I’ll be at the altar lol.

I think I’ll follow your resignation template if all is about the same between now and May. And yeah, the Ali’s at All Options Considered are great! They’re my chosen family 🥰

Oh, I thought one of them is your biological aunt lol! And Merry Christmas to you!

Merry Christmas to you too!!! 🎄🍺💝