How to Reach $100k Wealth on an Average Salary

We Want Guac is full of discussion about maximizing your income and lowering your expenses; there’s a massive reservoir of further financial resources out there to help you in your particular situation as a young adult with an average salary hoping for 100k. Sometimes you end before you even begin when you see folks touting their millionaire status, incredible houses, or bloated salaries.

“This seems so far off from where I am right now,” you might think to yourself, feeling creeping dread at the mountain before you. “These people are so intimidating and I don’t want to feel like I’m failing when compared to them. How can I ever even reach that level of wealth they have in the first place?”

The answer, of course, is by reaching six figures first. And reaching 100k can be done in your twenties on an average salary.

Your Salary and the Tax Rate

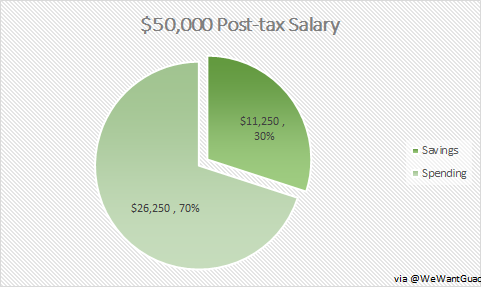

The Bureau of Labor Statistics puts the average wage at around $50,000 a year. You can definitely save and invest your way to $100k with that average salary WITHOUT taking on a side hustle or selling your firstborn to a sketchy forest witch.

First, you have to figure out how much money you’ll have. Let’s assume for easy math that you have a 25% tax rate on that $50,000. In reality your tax rate will be lower than this (which should make those six figs even more doable). This would leave you with $37,500 of after-tax income to use for your spending and your savings.

Once you know how much money you make, you can plan out how much to spend.

My general rule of thumb is to aim for a 30% savings rate, which in this case comes out to $11,250.

This means you’d have a little over $26k to spend per year ($26,250) which, I’ll be honest, will mean you’re living frugally. That’s what financial freedom requires, ain’t no getting around it unless you make a higher than average salary. But this doesn’t mean miserably-living-in-a-dumpster frugality; my own budget proves you can live large on a smaller budget as long as you optimize where your money goes.

If you’re attempting this in the Boston area, here’s what your monthly spending might look like:

| Expense | Cost |

| Studio or 1 bed rent | $1,200 |

| Utilities | $100 |

| Groceries | $150 |

| Phone bill | $60 |

| Miscellaneous/fun money | $300 |

All of the above would still leave you with about $4,500 to spare for whatever else your heart desires. This is also using Boston-area pricing, which is one of the most expensive places to live in the country. For me every single line item of the above, except for rent, is MORE than what I currently pay each year. You really don’t have to be a rockstar budgeter to do this; all you actually need is the desire to work for it.

Plus, who says you have to spend this much per year? You’re likely living in a cheaper part of the country where you can stretch your dollar much further. That means you can beef up your savings that much more and hit your wealth goals years earlier than projected. It doesn’t take much more to really knock this out of the park!

Once you’ve squared away your spending, you’re left with that nice savings rate of over $11,000 a year.

Here’s what to do with it.

Those five figure savings will get you to 100k much sooner on an average salary if you know how to best deploy it. That is NOT done by sticking it in a bank account and calling it a day. Thanks to our lovely friend Mr. Inflation, you’d be losing money in the long run by doing that.

| Age | Yearly Contribution | Year End Total (1.5% bank growth) |

| 22 | $11,250 | $11,419 |

| 23 | $11,250 | $23,009 |

| 24 | $11,250 | $34,773 |

| 25 | $11,250 | $46,713 |

| 26 | $11,250 | $58,832 |

| 27 | $11,250 | $71,134 |

| 28 | $11,250 | $83,619 |

| 29 | $11,250 | $96,292 |

| 30 | $11,250 | $109,156 |

Note that this chart assumes you’re receiving 1.5% interest, which few accounts actually offer. Most banks and credit unions out there do NOT give you so high an interest rate. Which is even worse than that 1.5%, because inflation generally eats away about 3% of your dollar’s value. Meaning, your ten dollar splurge this year will cost you $10.30 next year. This is why you want an investment return that will outpace inflation – any investment giving you a less than 3% return is LOSING YOU MONEY.

So you can’t just stick it in a bank account and let your savings rest. You need to put it to work.

Stick it In an Index Fund!!

We want to get double-digit returns on the money we’ve worked so hard to earn. The best way to do that is by placing them in index funds for an average market return of 10%. No stock picking here, as that brushes too close with straight-out gambling. Nuh uh, we want returns to be as safe as possible and will go this route for them. I prefer dumping all my money into VTSAX, aka the total stock market index fund offered by Vanguard. Other investment companies like Fidelity and Charles Schwab have their own version of VTSAX; do your research and choose whichever company floats your boat.

Because once you’re invested and having your money earn you more, THAT’S when you can call it a day. No need to further finagle with your index funds, not even when you see them “losing value”. That value isn’t actually lost unless you panic and sell, at which point you lock in that lower price forevermore. The stock market goes down on occasion, but historically always goes up. Leave it alone and give it enough time to grow for you.

And that time necessary isn’t actually that long at all. Here’s how much money you can expect to see with an average return of 10%:

| Age | Yearly Contribution | Year End Total (10% investment growth) |

| 22 | $11,250 | $12,375 |

| 23 | $11,250 | $25,988 |

| 24 | $11,250 | $40,961 |

| 25 | $11,250 | $57,432 |

| 26 | $11,250 | $75,551 |

| 27 | $11,250 | $95,481 |

| 28 | $11,250 | $117,404 |

See how much that accelerates?!

That’s less than seven years to reach $100k on your very average salary. If you get an average salary right out of college (unlike me) you’d reach 100k a year or two before your 30th birthday. That’s a lot of dough – enough to now match your $11k contributions in earnings every year and help you to a million dollars much more quickly.

Best part is, start young enough with that average salary and you don’t strictly have to continue saving. Hitting 100k in your investment accounts means you’ll be a millionaire retiree on that average salary without any extra effort. Then you can deploy that $11,000 you save to any other goal in the interim, whether that’s starting a family, buying a home, or going on an epic vacation every single year for the rest of your life.

Is this even doable?

In my case, I live on $30k a year with over $20k of that spent on rent alone. If I suddenly took a pay cut to $50k, I’d have to get a roommate for my 2 bed apartment. Which is doable. Or move into a cheaper apartment, which is also doable. Either way I’m still hitting that 30% goal easily in what is, again, one of the most expensive cities in the USA.

For the record, my current savings rate is right around 54% of my post-tax income; if you count my contributions to my 401k and HSA it’s 38%. And I still manage all of this while eating out and taking awesome trips (which are currently socially-distanced road trips). See, I take my own advice and it pays me HANDSOMELY to do so.

So poke around the site and others like it to figure out your own strategy towards incredible wealth. You’ve got a guide on your own climb to wealth, and that mountain isn’t as insurmountable as you thought.

Let’s get climbing.

this is about the same scenario i lay out in my malevolent missy investment series for beginners. maybe you’ve read it before. i gave our 20 something a 50k salary and similar expenses with 1000/month to invest. our twist is that she invests 3 different ways at those monthly intervals with her $1000. the first is she buys 1000 of vtsax. 2nd is she buys 1000 of qqq (nasdaq 100 index). 3rd is she buys a high quality stock. after 10 months of this her individual stock buys are up 40%. qqq is up 14%. vtsax is up 1.4%. we’ll see where it all ends up.

the real life missy is my coworker and she’s crushing it too but has a good teacher.

I’m still learning about investing. Is this something that could still be achieved if you just dump your money in a robo advisor like Wealthfront?

I haven’t personally used robo advisors myself, mainly because 1. it’s an extra fee eating into my investment growth that I don’t need because 2. I keep my investments stupid simple with index funds. In your case I’d say put some research into the investment brokerages out there (I’d recommend Vanguard) and their particular index fund offerings that track the overall stock market (I’d also recommend either VTI or VTSAX, which are pretty interchangeable).

At the end of the day though you should do whichever option makes you feel better about investing, because the most important thing right now is to get started. If you’re like me than you’d be dumping it all into VTSAX. If you’d sleep a little easier with something like Wealthfront then that’s a good option too; it looks like their 0.25% fee is more than reasonable and offers you some more assurance about this crazy thing you’re doing 😉