6 Reasons I’m Chill with Tariffs Wrecking My Investments

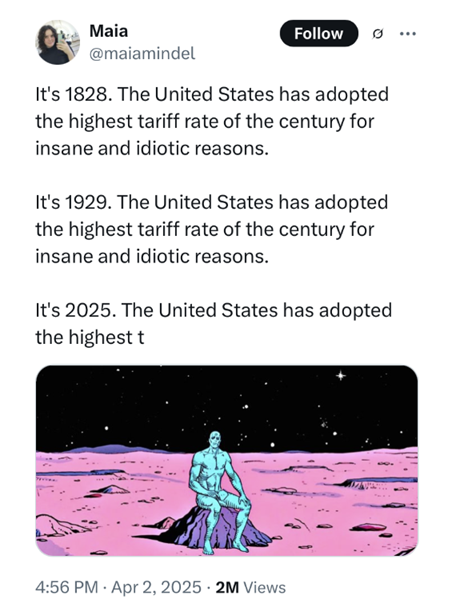

Tariffs suck and they have always sucked. “Tariff” is a synonym for “extra tax,” which I thought Americans were rather infamous for looking to avoid. (Looking at you, American Revolution. And you, main argument against universal healthcare.) But no! Tariffs will always be unpopular at best and will accelerate devastation and political upheaval at worst! This is a lesson the Founding Fathers had to navigate. After them, it was a lesson Americans had to keep relearning in the 1820s, the 1920s, and, apparently, the 2020s.

The 1820s extra tax was literally called the Tariff of Abominations. The 1920s one was widely criticized for exacerbating the Great Depression. This 2020s one, I hope, will make Trump voters recognize the error of their ways and repent with great wailing. Doubtful, but the hope is still there that the repenting will happen before widespread economic struggle does.

As of this moment, investors are the ones scrambling the most. The stock market is down over 7% YTD as of the time of this writing (April 14, 2025) and sees insane daily swings due to the frequent rollouts and rollbacks on tariff news. It’s a hassle to attempt to keep up with what’s going on and a recipe for disaster.

When it comes to how it affects meeeeeeee?

Well, it doesn’t.

At least, not in a way that will truly knock me down.

You wouldn’t think that by looking at my portfolio. Before all these tariffs upended the stock market, my net worth hovered in the $560k range. As of today, it’s around $507k. There are only two reasons why it’s still over half a million:

- I got a bonus in March and put most of it in my 401(k) during one of the stock market drops.

- Trump put in another pause on tariffs, so things will look good until he does something else stupid.

This is a scary, chaotic time. There have been plenty of times since November I’ve stared off into space and wondered if it’s more ethical to stay here or bounce to decidedly non-fascist Ireland. If I do bounce, should I start helping get my vulnerable loved ones over there too? I have a lot of plans in the spirit of “hope for the best, prepare for the worst,” but I don’t actually want those plans to be necessary for survival. As previous articles might suggest, I am a huge history buff with a ton of curiosity and also Internet access. I know what happens to countries consumed by fascism. I am not at all chill or serene about THAT.

What I AM feeling serene about, though, is my finances. Whenever I check in with myself about my portfolio gyrations, the only emotion there is “calm”. This is due to a number of reasons, going back to when I first started learning about finance in 2016:

1. My financial educators made it clear these black swan events WILL happen, so I made sure I was ready for ‘em.

When I was first teaching myself about the financial independence strategies and background research, the blogs I read were open and honest about something very important. Mainly, how you WILL see your portfolio drop 10-30% in some future dismal years. You HAVE to plan for that.

I was reading popular FIRE folks from the mid-2010s era; Mr. Money Mustache, Frugalwoods, JL Collins, and Millennial Revolution were my top picks. Every single one of them wrote about how their strategies were guaranteed to see dramatically negative years. Millennial Revolution has a great story about their panic and fear during the 2008 recession that they had to push through. Their sharing their experiences shaped my expectations for the better, strengthening my capabilities as an index fund investor.

Those black swan events didn’t mean their investment strategies stopped working; it is just due to the nature of the stock market that some years will be in the red. What gets you through is having faith in the research that the stock market will go back up (and stopping yourself from locking in your losses by selling). I took that to heart and built up my risk tolerance with that in mind. Going off that:

2. I worked on building my tolerance for risk/trusting the process.

Every investor risks their investment underperforming. You can mitigate that by diversifying with index funds (aka, NOT putting all your eggs into one basket/stock). However, that’s not guaranteed either if you sell at a loss before it can recover. I built my own risk tolerance by building confidence that what the FIRE writers were saying was true:

- That the stock market will go back up.

- That market crashes were part of the cycle and baked into the winning strategy.

- That it’s bounced back every single time from a plethora of crashing bubbles and pandemics and a couple World Wars.

- Also, index funds will never drop to $0, so the only way you’re walking away with nothing is if Armageddon happens… in which case, I will have very different problems to freak out about.

My risk tolerance was battle-tested during the COVID drop in 2020. Back then, my baby investments dropped 32% almost overnight. I still remember logging into Mint at the time, seeing that dramatic drop, and my only reaction being

“Oho! ( ͡° ͜ʖ ͡°) It’s happening just like they said it would!”

I also had a backup plan. If it turned out my risk tolerance was low, I would simply Not Look at how my portfolio was doing. Distraction is a valid coping mechanism, should you ever need it. I still keep that backup plan just in case, but 2025 has shown me my risk tolerance remains high. Which is great, because that means watching the S&P stock ticker is weirdly entertaining versus aneurysm-inducing.

3. I have a solid cash cushion/emergency fund.

Once upon a time (read: until last year) I was good with keeping a small amount of cash, preferring to chuck 99% of my money into investments. Now that my investments are large enough, I’m taking my big toe off the gas and keeping more than $2-5k in my bank account.

Right now, I’ve got $20k cash in the bank with a goal of maintaining $30k in the future. That feels extra safe and cushion-y to scrappy ol’ me, but it’s still just 4-6% of my overall net worth. You might feel the same level of security with a different amount of cash on hand; that’s all good, because your personal finance will be different from my personal finance. Which is relevant now, because I know I can live off the emergency fund-slash-cushion for up to a year without touching my investments. And that only comes into play if I also stop working. I’m good there, so no need to worry about my financial solvency at all.

4. I’m still working and, therefore, getting more money every two weeks.

Maybe I’d feel more nervous if I decided to retire back in January. Instead, I’m hanging onto my good marketing job and reaping the sweet, sweet financial benefits. Not only that, but I’m also taking advantage of my company 401(k) match in the process. The match is 5% per paycheck and I’m contributing 11%. That adds another cozy layer of security, since my portfolio will reap the rewards of buying up index fund investments at a lower price. “The stock market is on sale!” was a common rallying cry on this from FIRE yesteryears.

I like that I have choices to allocate that cash flow as necessary; if I decide to put more towards investments or go the opposite direction, I can do whatever I need to do for further peace of mind.

5. My portfolio will remain standing longer than Trump will remain in power.

This is my 2025 twist on the quote “The stock market can remain irrational longer than you can remain solvent”. The absolute worst Trump can do as Hitler 2.0 is leave America as Hitler did Germany: struggling hard for decades and rightfully, universally hated.

While I do think things are going to SUCK, as they already do for small business owners and the First Amendment, I sincerely doubt we will reach that endgame. My doubts are due to the sheer size of the US, making any big change slow-going, along with the sheer incompetence of this administration. (What do you mean, they don’t even have working tech to collect tariffs? Or open the Wikipedia page on History of tariffs in the United States?)

Americans are not known for their ruthless efficiency like Germans are, despite what propaganda would have you believe. Even the pessimistic side of me that hates oligarchy will begrudgingly admit that my index fund investments will mark me safe under oligarchy.

It might not seem so because I’m not a millionaire, but I still have over $500k to my name that’s invested in thousands of American businesses. (Thanks, index funds!) Unless every single one of those businesses goes bankrupt – including those businesses with a mammoth international presence – I will still have assets worth more than $0. Knowing that gives me the peace of mind that I will weather this storm. I will come out clean on the other side.

6. I don’t just have a Plan B. I have Plans A-X and can make more if needed.

Somewhere in my brain, I have a flow chart of what actions I will take to accomplish my hopes and dreams. If my status quo remains tentatively stable? Hold onto my job and reevaluate as needed. See progress with my dream of becoming a screenwriter? I’m taking it.

America goes full authoritarian state and a lot of my friends and loved ones are under threat? I’m moving abroad to an Irish castle in need of repairs. I will also request said loved ones come live with me to help renovate, who I can sponsor as an Irish citizen myself. (Dual citizenship was another such plan, and boy does it come in CLUTCH.) America goes full authoritarian, but no one needs to flee for some deus-ex-machina reason? World travels, here I come!!!

Remember when I mentioned I’ve still got a $500,000 net worth? That is still over my leanFI number. This means I have enough to live off of if I retire tomorrow, as long as I move somewhere with a low cost of living. The Earth Awaits says this covers several cities in Italy, where I can live no problem as an EU citizen. One of my worst options is a literal pipe dream for most. My work throughout my 20s has all but ensured my comfort, come what may.

Whatever happens, I trust myself and my capacity to handle it. Nothing is ever truly guaranteed in life, of course. But serenity sure comes natural when you have realistic and actionable plans to follow.

Final Note

I can yap through more points than that, but six is probably enough. The only other thing I can think to add is something I read from A Purple Life on Instagram about the 2025 craziness:

I’m a long term index fund investor so I care about what the market does over decades, not days.

I like that a lot. It’s a good reminder to zoom out and remember this won’t last forever. It ain’t over til it’s over.

Cover image credit: Teng Yuhong via Unsplash

Great article. Thank you. Good reminder to take the long view. Just wish these next 3.5 years would go faster.

You and me both. Otherwise, let’s do what we can.

I’m most concerned about the current threats to our constitutional rights. We have to stand strong for the freedoms that are core Americans values.

The current administration is testing the checks and balances in our system, using the dictator playbook, to see how much power he can wield.

We as citizens must stay vocal in our support of the constitution and of all of our public good programs under attack currently. And yet, the wannabe dictator in the white house may try to target innocents who try to defend the American constitution and American institutions. We know he is already targeting people in government who have opposed him, and legal residents who have not been charged with crimes are being wrongfully deported to the gulag in El Salvador (which we are paying for). Even natural born citizens are randomly getting letters saying they must self-deport (clearly in error, but not a good sign!).

Sorry this is a rant. I’m just very aware that my index funds may not be enough to save me if the current administration is allowed to really run amok. I don’t have dual citizenship. Since you do, I would also suggest you consider holding funds in Irish accounts, in case your U.S. accounts get frozen. I can’t believe I’m even saying that.

Absolutely no need to apologize, Morgan; if anything is worthy of a rant, it’s this. (Plus, my entire site is just me ranting about whatever I can connect to finance, so I’m the last person to cast a stone.)

I’m right there with you on the constitutional threats and your second paragraph is right on the money. In your third paragraph you say “the wannabe dictator in the white house may try to target innocents…” and I’d only edit the “may try to” to “will”. They’re already targeting some of the most prestigious, high-profile universities in the country, including that outrageous demand letter sent to Harvard they only just backed down about today. (Source)

I wish I had some surefire, widely applicable advice on how to survive a fascist state with your wealth and sanity intact. The FIRE investment strategy I advocate so strongly for is only as effective as it is because our constitutional rights prop up our economic prosperity. The most I can do is refer to what survivors of the Third Reich did to survive their own horrifying circumstances. (I, too, can’t believe I’m saying that.)

Having dual citizenship at all is a massive privilege that only a tiny fraction of people have. I’m traveling to Europe next month and will be testing how easily I can withdraw cash from an international bank I have accounts with. If I find it hard to do, I will very much be taking you up on your suggestion. If all else fails, at least my dual citizenship gives me the right to work for more. Not what I would want for myself, but still vastly preferable to many other life paths post-fascist state.

Can I request that you write about your experiences with international banking while abroad? I’m concerned about America going full tilt fascist and that the opposition party is more like the slightly less enthusiastically fascist party with some notable holdouts. Gavin Newsom can suck it, for one. I worry that the few highly visible holdouts (AOC, Sanders, Van Hollen, Walz) aren’t enough to derail this train of bad to worse.

I intend to stay and fight as long as we can but I’m also aware that things can get so much worse. Things are already unimaginably bad now, I spent the last two weeks trying to help stop a deportation and so have experienced a little of this administration’s destruction firsthand that way, so I have been researching where we might reasonably and legally hold some safety emergency money outside of the country in case they crash the US banking system.

I’m glad that you have the dual citizenship option. That gives you the ability to flee to safety and possibly help others, too. I’m not sure what our escape hatch plan might look like but I understand that it’ll be a great deal harder than uninformed people realize. No one is going to want to accept a horde of Americans. Much like Americans who loathe refugees and immigrants, the irony is loud and clear.

Hi Revanche, I’m so happy to see your comment and sad I cannot make things much better. I now have an article on international banking coming. It might take some time because I’ve got a lot going on right now, but definitely within the next few months.

In the meantime, I can recommend looking into Santander Bank as an option. When I was studying abroad in Madrid in 2014, my classmates overwhelmingly used Santander as they could use it both in Spain and in the US. For my wealthy classmates, it sure helped to have their parents able to fund their bank account from home while they were overseas. Google tells me this is still the case for Santander, but I’ll need to do some actual research to be sure.

I very much agree that my dual citizenship is my ace-in-the-hole during political shakeup. I heard radio chatter outside my apartment today and rushed to my balcony, thinking that there was an ICE van outside and I’d need to run down and gather names and birthdays from those taken away. It wasn’t ICE, but that remains a looming possibility. The biggest problems on my street should be drunk clubgoers and bad parking, not the reincarnation of the Nazi SS. It’s awful times that promise to only get worse from here.

Pingback:Good Things Friday (327) and Link Love « A Gai Shan Life