What if Financial Independence Goes Wrong?

We are now in month 2 of my cross-country road trip and month 5 of my voluntary unemployment. If I was in my 60s, nobody would bat an eye at this. Since I’m in my early 30s, however, this raises quite a few brows.

The naysayers who pooh-pooh my plans have a much less rosy outlook on this time of my life than I do. They ask me about spending projections, long-term economic crashes, and what I’m gonna do if I run out of money. At the core, these negative reactions have one common thread of worry: what if financial independence all goes wrong? What if an early retirement (which I’m not sure I’ll do yet) turns out to be a mistake?

These are valid questions, as financial independence is the standard marker between “working for a living” and “not working for a living”. If you lose your job – and, therefore, your source of income – then the strategy is to find another job or some other way to bring in money. When your source of income is from investments instead of labor, the equation looks different. I don’t have to worry about job loss, career shakeups, toxic workplace culture, or bad management directives any longer.

I have exchanged all of those worries for one main one: sequence of returns risk (SORR).

What Is SORR?

The risk here is: my portfolio is enough to sustain me for the rest of my life, unless my investments deliver negative returns for the first few years. If that happens, theoretically, then I will end up withdrawing money from a portfolio already low in value. That has a domino effect through the years. Without enough time to recover its value, it’s possible to go broke entirely in another couple decades.

And if that were to happen, I’d certainly struggle to find a high-paying job given I was out of the labor market for so long. What job skills would I have that wouldn’t be stagnated, or expertise on tools that’s twenty years out of date? The best I might hope for would be low-paying jobs that people with mush for brains dub “unskilled”.

SORR presents real concerns here.

It’s also so much of a better deal that it’s absurd.

Were I to lose my job when I still needed one, it would be a race against the clock to find something else. Can’t have too big of a gap between jobs, after all, or that reflects badly on my chances of getting hired. I run a real risk of accepting a role at an organization that isn’t healthy to be at; grinding it out at a toxic workplace is much better for the resume, if not your health. And what recourse do I have for the drawbacks of corporate that make up the standard experience? There’s no escaping the stale networking events, boring meetings, dramatic coworkers, conferences with little tangible value, and – worst of all – the commute.

The vast majority of workers are nowhere near lucky enough to snag a full-time remote position. At minimum, they have to balance waking up early, dealing with traffic that could result in a car accident every day, and all without the cultural norm guaranteeing they get back home at a reasonable time.

After experiencing all of that, I am over the moon that I get to opt OUT of all of that. Instead of dealing with all that nonsense, all I have to do is properly mitigate SORR. That is a done deal; my signature is already dried on the paperwork and my hand is out to shake on it. SORR is SO much more easily accounted for with the appropriate guardrails. Now that I have those guardrails in place and additional contingency planning, all of this makes financial independence all but secure.

Darcy’s Financial Independence Guardrails

My own guardrails are straightforward and ridiculously easy to manage. I was already doing all of this while employed without issue, so doing it now is second nature. In no particular order:

Check on net worth weekly

If I’m seeing a shaky portfolio over a long period of time, I can consider adjusting if need be. So far, my net worth has gone up from $700k to about $733k, which means I could safely withdraw $30k at 4.1% (link to why I go a little over the 4% rule). However, if that number goes down – and stays down for a year plus – that will be my first warning to adapt before issues further down the road.

Use budget measure as the ceiling, not as goal spend

My “instinctive” approach to spending money is to hoard it, which stems from unhealthy childhood survival skills. I know how to keep this in check as a seasoned adult, but I can also recognize it can be useful in this narrow circumstance in moderation.

Keep a cash cushion

Shoutout to Millennial Revolution for their great breakdown on the cash cushion. I have about $30k in cash, most of which is park in a high yield savings account. Since I’ve already paid for most of my housing for the rest of the year (thanks, Airbnb!) this will last me for at least the next 1.5 years. Barring some emergency, projections say I won’t exhaust this until January 2028.

Monitor cash infusions coming in

That cash cushion above isn’t counting cash infusions in the meantime. Since I invest in stock market index funds – which, by nature, include dividend stocks – I’m expecting a few thousand in dividends every year from my taxable account alone. I also own some equity in a healthtech company (my former employer!) that has generated quarterly payouts for the last few years. I include that here as, in years past, it’s been enough of a boost to move the cash needle.

Darcy’s Contingency Plans

All of my above guardrails are fine and dandy. You may have noticed my phrasing of “I can consider adjusting if need be”. My wording here is very deliberate. It’s always possible that we experience a second Great Depression, which saw the stock market return negative 89% in a four-year time frame (1929-1932). If financial independence was to go wrong, this is the most likely scenario to make it so.

That would be the case, if, of course, I didn’t already have contingency plans in place for this! I only ever get burned when I don’t have backup plans “just in case,” and so I know what my strategy will be in this scenario as well.

- If less than 20% drop: continue drawing down from cash and crypto and taxable.

- If 20-30% drop: this is what the cash cushion is for 🙂 Keep an eye on investment performance and see how things shake out in another 1-2 years.

- If 30-50% drop: implement spending floor of $22,200 yearly spend. This supports a monthly spend of $1,850. I can easily meet this by just chilling around Italy, Greece, and Spain, as I calculated here. I used cFIREsim to run some Monte Carlo simulations, and using this as my spending floor showed a 100% success rate!

- If more than a 50% drop over multiple years: should this be the case after four years of financial independence, I will be in my mid-30s and much more relaxed than the average person, having enjoyed multiple years of travel around the world. That is a perfectly fine time to consider reentering the labor force on my own terms; whether I get a job that uses my high-value skills or my more basic ones, my critical thinking skills and pleasant demeanor will get me something to tide me over. Add to that the benefit of coming in with zero burnout or compounded stress from the previous four years of economic carnage, and I can navigate the economic recovery much more calmly than most.

Best of all, SORR will not happen to me suddenly. I’ll be able to see it coming a mile away. Actually, more like a hundred miles away. This is not a problem that will catastrophize overnight; there will be plenty of time to consider my options and course-correct.

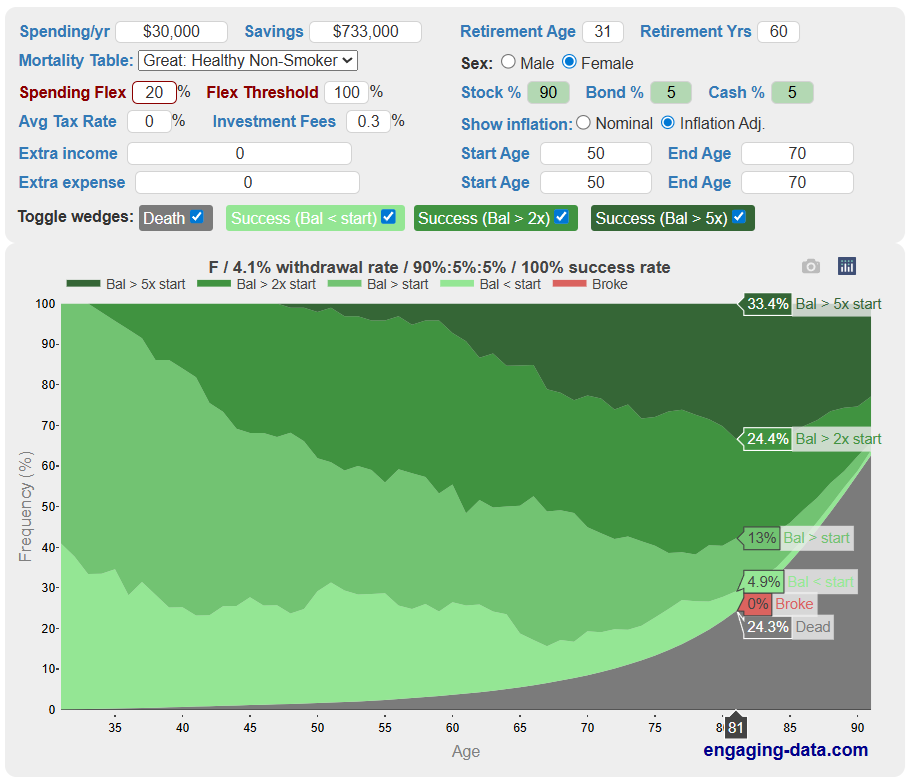

My Chances of Success are All But Assured

Besides cFIREsim, I’ve also played around with other online calculators to determine my chances of success. Interestingly, the Rich, Broke, or Dead calculator estimates that my chances for success are already at 100%. What sweetens the pie further here is that this isn’t accounting for Social Security; I have enough Social Security credits to gain additional monthly payouts as early as 62. Without the Social Security buffer, the specific breakdown for fifty years of FIRE is:

- A 57.8% chance my net worth is double (or quintuple!) the starting balance

- A 13% chance my net worth is the same as it was at the start

- A 5% chance my net worth is less than it is right now

- A 0% chance I’ll be BROKE!

- And a 24% chance I’ll be dead

The above is using the above-average mortality tables; I’m physically fit as a fiddle, and all four of my grandparents lived long lives despite hard childhood struggles. If my lifespan is more average, then that makes my financial independence even better by increasing my quality of life right now. Even if my chances of success weren’t at 100%, I’ll still take it knowing that risk. Which, for the record, is a deal I actively AM taking.

I’m writing this in a library in Tulsa before swanning on to Arkansas and beyond. Pursuing financial independence has been the best decision of my life, and I’m so glad I have the guardrails and plans in place to ensure I enjoy it in the decades to come.

Cover image credit: ME! This is from outside the convention center in Tulsa, OK!

You go Darcy, live ur life and trust the process. I’m positive things will work out just fine for you. You are a high achiever, so even if you decide to work in the future, you won’t have a problem making more money.

Thanks so much for this! 🥹

Curious what % of your NW is in taxable/cash/tax deferred/Roth buckets and how you are navigating that?

Hi Jon, sure thing! I have about $30k in cash and $230k in taxable, which is roughly 35% of my net worth; depending on market fluctuations, that amount alone should see me through the next 10-15 years without counting extra income streams like dividends. After that, I’ll either fund my lifestyle via the Roth conversion ladder (currently about $130k in there, so projecting ~$400k with 15 years of growth) or the 72(t) approach with my 401(k) (currently around $295k). The 72(t) approach is likely the best for my specific needs, but we’ll see several years from now! And if you’re interested in early retirement withdrawal strategies, I highly recommend this article on the topic from All Options Considered. They’re fantastic!